TL;DR:

- Insurance-free healthcare is gaining popularity in 2026, offering direct payments, memberships, and community programs as affordable alternatives to traditional insurance. Models like Direct Primary Care, cash-pay clinics, and sliding-scale programs provide predictable primary care costs, but major medical events still pose significant financial risks. Patients should layer primary care options with catastrophic coverage and understand program limitations to effectively navigate coverage gaps.

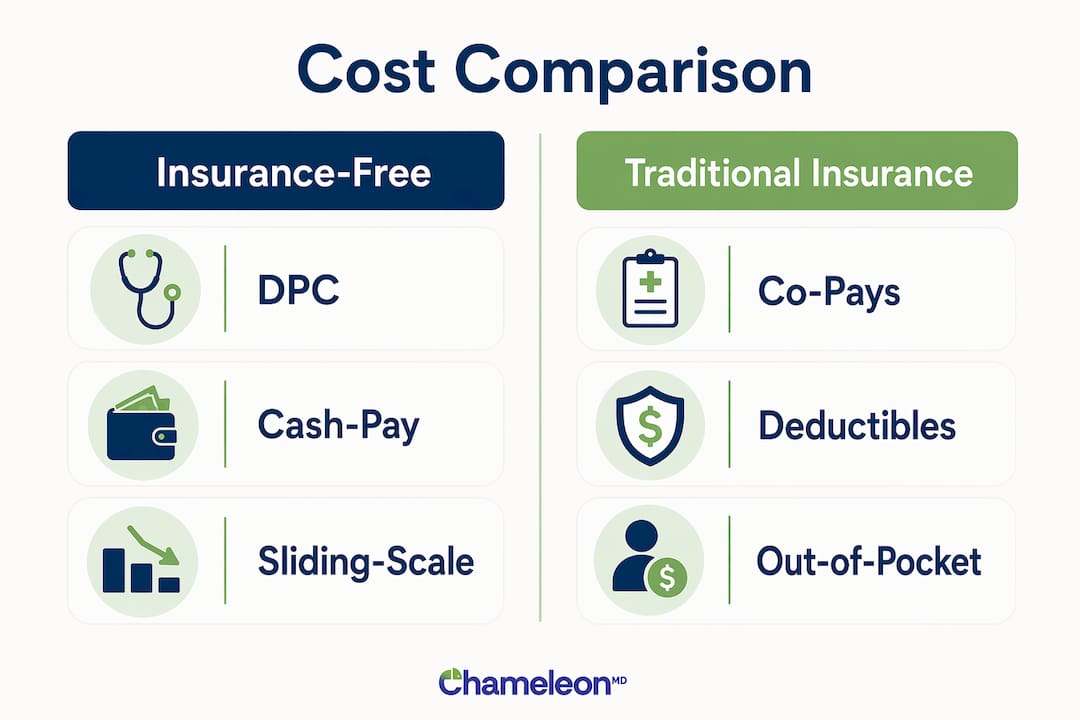

Insurance-free healthcare is defined as accessing medical services without using traditional health insurance, relying instead on direct payments, membership models, and community programs to cover the cost of care. This approach is gaining real traction in 2026, and for good reason. 61.7% of uninsured adults cite unaffordable coverage as their primary reason for going without insurance, and 38.6% have delayed or skipped care entirely because of cost. That data tells a clear story: the traditional insurance model is leaving millions of people behind. Programs like NYC Care, Direct Primary Care (DPC) memberships, and cash-pay clinics are filling that gap with practical, affordable alternatives that put care back within reach.

Insurance-free healthcare explained: the main models

Understanding insurance-free care starts with knowing which models exist and how each one actually works. These are not workarounds or last resorts. They are structured systems designed to deliver real medical care at predictable prices.

Direct Primary Care (DPC)

Direct Primary Care operates on a monthly membership fee, typically between $50 and $150, paid directly to a primary care provider. In exchange, you get unlimited primary care visits, same-day or next-day appointments, and direct access to your doctor by phone or message. There is no insurance billing, no co-pays, and no surprise charges for routine visits. The 2026 update worth knowing: DPC memberships are now eligible for pairing with Health Savings Accounts (HSAs) under certain plans, making them more financially flexible than before. The key limitation is that DPC does not cover hospitalizations, specialist referrals, or emergency care.

Cash-pay clinics and direct lab ordering

Cash-pay clinics charge a flat, transparent fee for each visit. You pay at the time of service, and the price is posted upfront. Patients choosing cash-pay report shorter wait times and far less billing complexity compared to insured visits. Direct lab ordering services like Labcorp OnDemand and Quest Diagnostics allow you to order your own blood work without a referral, often at a fraction of the insured price. This model works well for people who need routine diagnostics or treatment for common conditions without the overhead of insurance processing.

Sliding-scale and community health programs

NYC Care is one of the most cited examples of a sliding-scale program, offering primary care starting at $0 based on income and residency in New York City. Federally Qualified Health Centers (FQHCs) operate on a similar model nationwide, adjusting fees based on your income and family size. These programs are not entirely free for everyone, but they are designed to make care affordable rather than free-on-paper-but-inaccessible-in-practice.

| Model | Monthly Cost | What’s Included | Key Limitation |

|---|---|---|---|

| Direct Primary Care | $50–$150 | Unlimited primary care, direct provider access | No hospital or specialist coverage |

| Cash-pay clinic | Per-visit fee | Diagnosis and treatment for common conditions | Costs vary; no ongoing care relationship |

| Sliding-scale / FQHC | $0–variable | Primary care, some preventive services | Income verification required; limited scope |

| NYC Care | $0–low fee | Primary care, essential services | NYC residents only |

Pro Tip: If you are considering a DPC membership, ask the provider specifically what is included in the monthly fee versus what triggers an additional charge. Lab work, imaging, and specialist referrals are often outside the membership scope.

How does accessing healthcare without insurance affect costs and care quality?

The financial picture of healthcare without insurance is more nuanced than most people expect. The benefits are real, but so are the gaps.

On the cost side, insurance-free models often deliver more predictable pricing for primary care. A DPC membership gives you a fixed monthly cost. A cash-pay clinic posts its prices before you walk in. That transparency is something traditional insurance rarely offers, where the final bill can arrive weeks later and bear little resemblance to what you were quoted. Uninsured patients carry a 34% rate of unpaid medical bills, which reflects not just inability to pay but also the shock of unexpected costs. Predictable pricing reduces that risk significantly for routine care.

The patient experience also improves in measurable ways. Fewer administrative barriers mean less time on hold, less paperwork, and faster access to a provider. Cash-pay and direct care models reduce the friction that makes people put off care until a problem becomes serious.

The gaps, however, are significant and worth naming clearly:

- Emergency and hospital care is not covered by DPC or cash-pay models. A single hospitalization can cost tens of thousands of dollars out of pocket.

- Specialist visits such as cardiology, orthopedics, or dermatology are typically outside the scope of DPC and sliding-scale programs.

- Prescription costs vary widely and may not be discounted under cash-pay arrangements unless you use a tool like GoodRx.

- Chronic condition management requiring frequent specialist oversight can become expensive without any coverage layer.

The practical takeaway is that insurance-free care works best as a primary care solution. For major medical events, the financial exposure without any coverage can be severe.

| Care Type | Insurance-Free Cost Range | Insured Out-of-Pocket (Estimate) |

|---|---|---|

| Primary care visit | $50–$150 (or DPC membership) | $20–$50 co-pay |

| Blood panel (direct lab) | $30–$100 | $0–$50 after deductible |

| Emergency room visit | $1,500–$3,000+ | $150–$500 co-pay |

| Specialist visit | $150–$400+ | $50–$150 co-pay |

What legal protections and patient rights exist for uninsured individuals?

Being uninsured does not mean being without rights. Federal law is clear on this point.

Federal law requires hospitals to provide emergency stabilization to any patient regardless of insurance status or ability to pay. This is mandated under the Emergency Medical Treatment and Labor Act (EMTALA). Hospitals cannot turn you away from an emergency room because you lack coverage. What EMTALA does not cover is the bill that follows. Once you are stabilized, the financial responsibility for non-emergency follow-up care falls to you.

Here is what you can do to protect yourself financially:

- Request an itemized bill. Billing errors are common, and an itemized statement lets you identify and dispute incorrect charges.

- Ask about charity care. Most nonprofit hospitals are required to offer financial assistance programs. Ask the billing department directly before assuming you owe the full amount.

- Negotiate a payment plan. Hospitals routinely accept installment arrangements. A payment plan prevents the bill from going to collections while you manage the cost over time.

- Apply for prompt-pay discounts. Some providers offer a reduced total if you pay a lump sum quickly. This is worth asking about before you set up a payment plan.

- Screen for program eligibility. Uninsured patients can access free or sliding-scale programs including county assistance, clinical trials, and school-based clinics. The Patient Advocate Foundation maintains a resource directory for exactly this purpose.

Pro Tip: Before your first visit to a sliding-scale clinic or FQHC, gather your proof of income (pay stubs or tax returns), proof of residency, and a valid ID. Having these documents ready speeds up enrollment and gets you to care faster.

How to find and qualify for insurance-free healthcare programs

Locating the right program takes a few deliberate steps, but the process is more straightforward than most people assume.

- Start with HRSA’s health center finder. The Health Resources and Services Administration maintains a searchable database of FQHCs at findahealthcenter.hrsa.gov. Enter your zip code to find the nearest sliding-scale clinic.

- Check city and county programs. NYC Care is one example, but many cities and counties run their own low-income care programs. Search your city’s official health department website for current enrollment details. NYC Care requires proof of NYC residency and income documentation, and the process can be completed online or in person.

- Verify covered services before enrolling. Sliding-scale programs at FQHCs have contractual limits on which services qualify for discounted fees. Confirm that the specific care you need falls within the program’s scope before your first appointment.

- Research cash-pay clinics in your area. Search for urgent care centers that advertise self-pay pricing. Call ahead to confirm the posted price covers the full visit, including any tests or prescriptions discussed during the appointment.

- Look into telehealth options. Telehealth platforms that operate on a flat-fee or subscription model are among the most accessible forms of affordable care without insurance. They eliminate travel time, reduce wait times, and often cost less than an in-person cash-pay visit for common conditions.

- Ask about free screenings. Community health fairs, pharmacy clinics, and nonprofit organizations frequently offer free blood pressure checks, diabetes screenings, and STI testing. These are legitimate entry points into a broader care relationship.

The benefits of preparation here are real. Patients who arrive at a sliding-scale clinic with the right documentation are enrolled faster and experience fewer delays in receiving care.

Key takeaways

Insurance-free healthcare works best as a layered strategy: direct primary care or telehealth for routine needs, combined with catastrophic coverage or charity care access for major medical events.

| Point | Details |

|---|---|

| Core definition | Insurance-free care uses DPC, cash-pay, and sliding-scale models instead of traditional insurance. |

| Cost predictability | Flat fees and memberships make routine care costs transparent, unlike traditional insurance billing. |

| Legal protections | Federal law guarantees emergency stabilization regardless of insurance status under EMTALA. |

| Program access | FQHCs, NYC Care, and county programs offer income-based care; documentation speeds enrollment. |

| Key gap to plan for | DPC and cash-pay models do not cover hospitalizations or specialists; plan for major medical events. |

What I’ve learned about going insurance-free in 2026

The most common mistake I see people make when exploring insurance-free options is treating it as an all-or-nothing decision. They either keep expensive traditional insurance they can barely afford, or they drop coverage entirely and hope nothing serious happens. Neither approach is sound.

The smarter path is layering. A DPC membership or a telehealth subscription handles your day-to-day primary care at a predictable monthly cost. A catastrophic insurance plan, which carries a low premium and a high deductible, covers you if something major happens. That combination often costs less than a standard insurance premium while leaving you with better access to routine care. Self-employed individuals and small business owners, in particular, benefit from exploring these hybrid models before defaulting to the ACA marketplace.

What most articles miss is the importance of understanding program limitations before you need care. Sliding-scale programs are not blank checks. They cover specific services, and anything outside that scope is billed at standard rates. Patients who discover this mid-treatment face exactly the kind of financial shock these programs are supposed to prevent.

The trend toward insurance-free and hybrid care is not slowing down. Telehealth adoption, direct lab access, and transparent pricing are reshaping what patients expect from healthcare. The people who navigate this well are the ones who treat their healthcare like a financial plan: they know what they have, what it covers, and what they would do if something unexpected happened.

— Vector

How Chameleonhc supports insurance-free healthcare

If you are looking for fast, affordable care without the paperwork, Chameleonhc is built for exactly that. You connect with a licensed provider online, get a diagnosis, and receive a treatment plan the same day. No insurance required, no waiting room, and no surprise bills.

Chameleonhc covers a wide range of common conditions, from asthma management to sprains and strains, all through a simple telehealth visit. The virtual care plans are designed to give you ongoing access to care at a flat, transparent price. For anyone building an insurance-free healthcare strategy, Chameleonhc fills the primary care gap with the speed and clarity that traditional systems rarely deliver. You can also explore telemedicine’s cost advantages to see how telehealth fits into a broader affordable care approach.

FAQ

What is insurance-free healthcare?

Insurance-free healthcare is medical care accessed without traditional health insurance, using models like Direct Primary Care memberships, cash-pay clinics, and sliding-scale community programs to cover costs directly.

How does Direct Primary Care work without insurance?

DPC charges a monthly membership fee of $50 to $150 for unlimited primary care visits with no insurance billing, though it does not cover hospitalizations or specialist care.

Are uninsured patients protected in emergencies?

Federal law under EMTALA requires hospitals to provide emergency stabilization to all patients regardless of insurance status, but non-emergency follow-up care remains the patient’s financial responsibility.

How do I qualify for sliding-scale healthcare programs?

Programs like NYC Care and FQHCs require proof of income, residency, and family size to determine your fee tier. Gathering these documents before your first visit speeds up enrollment significantly.

Is insurance-free healthcare a good long-term strategy?

It works well for routine and primary care, but the risk of medical debt is real for uninsured adults facing hospitalizations or emergencies. Pairing a DPC or telehealth plan with catastrophic insurance provides the most financial protection.