TL;DR:

- Over a third of adults avoid medical care due to costs, making affordable urgent care essential.

- Affordable options include self-pay clinics, retail clinics, telehealth services, and federally qualified health centers.

- Urgent care is suitable for non-emergency conditions, but serious issues require emergency room treatment.

Over a third of adults skip medical care because of cost. If you’ve ever hesitated to see a doctor because you weren’t sure what the bill would look like, you’re not alone. Affordable urgent care refers to walk-in or virtual medical services designed to treat common, non-emergency conditions at a price that doesn’t require insurance or a savings account to manage. This guide breaks down what these options actually cost, where to find them, and how to use them safely so you can get the care you need without the financial stress.

Table of Contents

- Defining affordable urgent care: What makes it ‘affordable’?

- Where to find affordable urgent care: Types and locations explained

- When urgent care is (and isn’t) the right choice: Risks, limits, and alternatives

- How to save even more: Smart tactics for cutting your urgent care bill

- Why affordable urgent care is changing healthcare for everyone

- Affordable urgent care made even easier with Chameleon

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Affordability defined | Affordable urgent care usually means self-pay options with lower fees, and community clinics can offer care for as little as $0 to $50. |

| Smart location choice | Choosing walk-in, telehealth, or sliding-scale clinics can keep costs far below the ER for common health needs. |

| Know your options | Urgent care is safe for minor and non-life-threatening conditions, but emergencies should go to the ER. |

| Cost-saving actions | Negotiating prices, using payment plans, and leveraging telehealth can all further reduce your bill. |

Defining affordable urgent care: What makes it ‘affordable’?

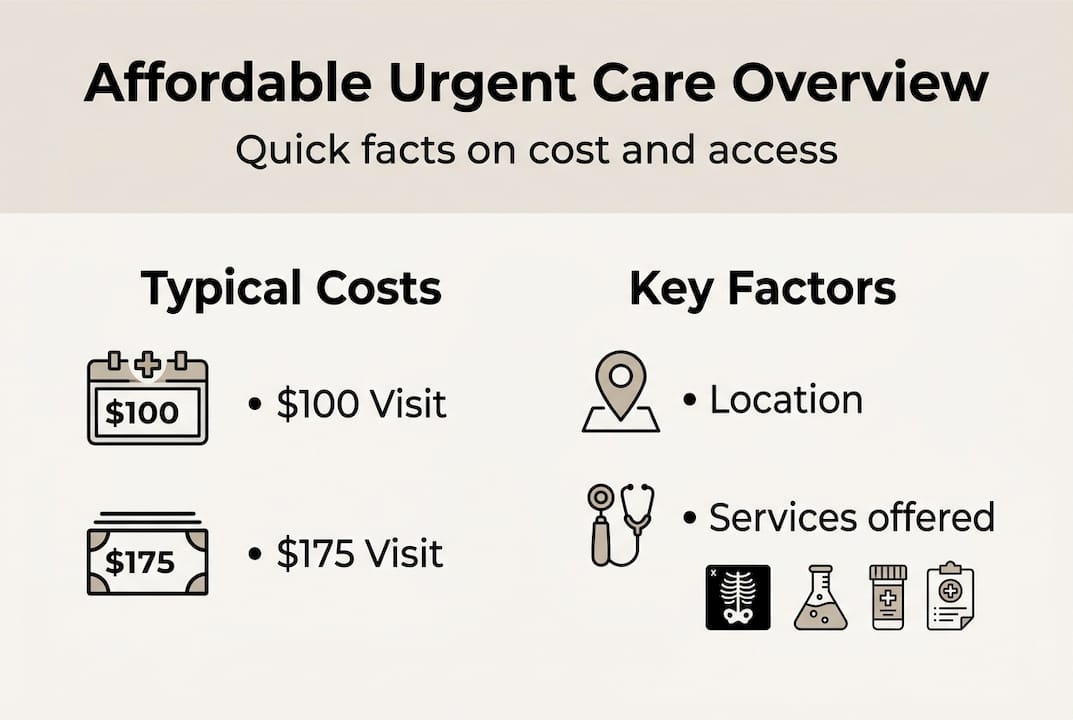

Not all urgent care is created equal, and the word “affordable” gets used loosely. For someone without insurance, affordable urgent care means a medical visit where you pay a clear, manageable fee out of pocket, without surprise charges or a bill that arrives weeks later.

Standard urgent care centers typically charge between $100 and $175 for a basic self-pay visit. That’s a wide range, and costs can climb higher if you need lab work, imaging, or a prescription. Emergency rooms, by comparison, often start at $500 to $1,500 or more for a visit, even for minor issues. Primary care offices can run $150 to $300 for a new patient without insurance.

The most genuinely affordable options are Federally Qualified Health Centers, or FQHCs, and community health clinics. These facilities use a sliding-scale fee model, meaning your cost is based on your income. For uninsured patients, sliding-scale fees at FQHCs can range from $0 to $50 per visit. That’s not a typo. Some visits cost nothing at all if your income qualifies.

| Care type | Typical self-pay cost | Insurance required? |

|---|---|---|

| Emergency room | $500 to $1,500+ | No, but highly recommended |

| Standard urgent care | $100 to $175 | No |

| Retail/pharmacy clinic | $80 to $150 | No |

| Telehealth urgent care | $30 to $99 | No |

| FQHC/community clinic | $0 to $50 | No |

Keep in mind: The cost of your visit doesn’t always include labs, X-rays, or medications. Always ask what’s included in the quoted price before you agree to any service.

Location plays a big role in pricing. Urban clinics in high-cost areas tend to charge more. Clinics with on-site labs or imaging will often bill separately for those services. Transparent pricing, where the clinic posts rates upfront, is one of the clearest signs you’re dealing with a genuinely affordable option. You can explore affordable healthcare options in more detail to get a fuller picture of what fits your situation.

Where to find affordable urgent care: Types and locations explained

With clarity on what makes care affordable, let’s look at real locations and types where you can find these services.

Walk-in urgent care centers are the most recognizable option. They’re often open evenings and weekends, accept self-pay patients, and can handle a wide range of conditions. Costs vary, but many post self-pay rates online.

Retail clinics, found inside pharmacies like CVS or Walgreens and some grocery stores, are another solid choice. They’re staffed by nurse practitioners and physician assistants, and they typically handle straightforward issues like strep throat, ear infections, and minor skin conditions. Prices are usually lower than standalone urgent care centers.

Telehealth urgent care has grown significantly and is often the most affordable and convenient route. You connect with a licensed provider from your phone or computer, often within minutes. Many platforms charge $30 to $75 per visit, with no travel time or waiting room. If you’re dealing with telehealth for urgent symptoms, this is worth exploring first.

FQHCs and community health centers serve patients regardless of insurance status or ability to pay. Sliding-scale fees make these the lowest-cost option for many uninsured individuals. You can find one near you through healthcare.gov or your local public health department.

| Care type | Hours | Self-pay friendly? | Best for |

|---|---|---|---|

| Walk-in urgent care | Extended hours, weekends | Yes | Infections, injuries, minor illness |

| Retail clinic | Store hours | Yes | Simple infections, vaccines |

| Telehealth | 24/7 in many cases | Yes | Rashes, sore throat, sinus issues |

| FQHC/community clinic | Weekday, some evenings | Yes, income-based | Ongoing or low-income care |

Conditions commonly treated at these locations include:

- Sore throat and strep

- Sinus infections and congestion

- Ear infections

- Urinary tract infections (UTIs)

- Minor cuts and wound care

- Rashes and skin irritation

- Coughs and cold symptoms

- Pink eye

Knowing which type of clinic fits your condition can save you time and money before you even walk in the door.

When urgent care is (and isn’t) the right choice: Risks, limits, and alternatives

Even with accessible options, it’s crucial to know when urgent care is the right fit and when to look elsewhere.

Urgent care is designed for conditions that need prompt attention but aren’t life-threatening. Think of it as the space between a routine doctor visit and a true emergency. It works well for infections, minor injuries, and sudden but manageable symptoms. What it can’t do is handle serious emergencies safely.

Go to urgent care for:

- Sore throat or suspected strep

- Ear or sinus infections

- Minor cuts that may need stitches

- Sprains and strains from minor injuries

- UTIs and bladder infections

- Mild to moderate asthma attacks with a known history

- Skin rashes without systemic symptoms

- Nausea, vomiting, or diarrhea without severe dehydration

Go to the ER for:

- Chest pain or pressure

- Difficulty breathing or shortness of breath

- Signs of stroke (sudden numbness, confusion, vision changes)

- Severe allergic reactions

- Heavy or uncontrolled bleeding

- Loss of consciousness

- High fever in infants under three months

For uninsured patients, the financial stakes are real. Uninsured patients face higher out-of-pocket costs than insured patients at urgent care, but the bill is still significantly lower than an ER visit for the same issue. Self-pay patients also miss out on negotiated insurance rates, which means being informed before you go matters.

For many non-urgent issues, a community clinic or telehealth visit is both safer on your wallet and just as effective medically. You can read more about managing costs without insurance to plan ahead.

Pro Tip: Before agreeing to any service at an urgent care center, ask for a written estimate. Most clinics are required to provide one, and it gives you the chance to compare options or negotiate before you’re handed a bill.

How to save even more: Smart tactics for cutting your urgent care bill

Once you know where and when to get care, these tips can make your visit even easier on your wallet.

The first move is to ask directly. Many urgent care centers have a self-pay discount that isn’t advertised. Simply saying “I’m paying out of pocket, do you have a self-pay rate?” can reduce your bill by 20% to 40% in some cases. It feels awkward the first time, but it’s a completely normal ask.

Urgent care spending has increased substantially over the past five years, which means clinics are more motivated than ever to retain self-pay patients. That gives you more leverage than you might expect.

Here are practical ways to reduce your bill:

- Use telehealth first for conditions that don’t require a physical exam. It’s often the cheapest option and available same day.

- Choose FQHCs if your income qualifies. The sliding-scale model is the most reliable way to pay little or nothing.

- Ask about payment plans before leaving the clinic. Many facilities will split a bill into monthly payments without interest.

- Request an itemized bill after your visit. Errors are common, and you can dispute charges you don’t recognize.

- Look into financial assistance programs. Hospitals and community clinics often have charity care funds that aren’t widely advertised.

- Compare prices before you go. Some areas have price transparency tools online, and telehealth platforms post their rates clearly.

Pro Tip: Ask the clinic for a universal billing slip (also called a superbill) after your visit. This document lists all services with billing codes and can be used to negotiate your bill later or apply for reimbursement if you get insurance in the future.

You can also explore affordable health tips and virtual urgent care options that make it easier to stay on top of your health without overspending.

Why affordable urgent care is changing healthcare for everyone

Here’s something worth sitting with: affordable urgent care isn’t just a workaround for the uninsured. It’s exposing a structural gap that has existed in American healthcare for decades.

The growth in urgent care use tells a clear story. Utilization increased 35% from 2018 to 2022, and spending rose even faster. People aren’t choosing urgent care because it’s perfect. They’re choosing it because primary care is inaccessible, expensive, and slow. Urgent care fills that gap, but it also creates a new risk: using it as a substitute for ongoing care rather than a supplement to it.

The smartest approach is to treat urgent care as one tool in a broader strategy, not the whole toolbox. Telehealth, community clinics, and direct-pay models each serve a different need. When you understand what most people miss about urgent care costs, you start making choices that protect both your health and your finances over time. Affordable urgent care is a real solution, but it works best when you use it intentionally.

Affordable urgent care made even easier with Chameleon

If you’ve been putting off care because you weren’t sure what it would cost or how to access it, Chameleon Healthcare makes that decision a lot simpler.

With Chameleon, you can connect with a licensed provider from your phone or computer, same day, with transparent pricing and no insurance required. Whether you’re dealing with a sore throat, a sinus infection, a rash, or another common condition, you can see conditions we treat and get started right away. For ongoing care needs, virtual care plans offer a membership-based option that keeps costs predictable and access easy. Getting care shouldn’t feel like a gamble. With Chameleon, it doesn’t have to.

Frequently asked questions

What counts as ‘affordable’ urgent care if I have no insurance?

Affordable urgent care typically means walk-in, community, or telehealth clinics where self-pay visits range from $0 to $175, with true low-cost options like FQHCs charging as little as $0 to $50 based on your income.

Is urgent care really cheaper than the ER if I’m paying cash?

Yes. For non-emergencies, urgent care is almost always significantly cheaper than the ER, even without insurance. Uninsured patients still pay less at urgent care than they would for the same issue treated in an emergency room.

Can urgent care treat all medical problems?

No. Urgent care handles common, non-life-threatening conditions like infections, sprains, and minor asthma episodes well, but chest pain, heavy bleeding, or stroke symptoms require an emergency room immediately.

How can I find a sliding-scale clinic or community health center?

You can search for Federally Qualified Health Centers near you through healthcare.gov or by contacting your local public health department directly for a referral.

Are payment plans or financial aid available for urgent care bills?

Yes. Many urgent care centers, FQHCs, and community clinics offer payment plans or financial assistance programs. Sliding-scale clinics in particular are designed to work with patients who can’t pay the full cost upfront.