TL;DR:

- A primary care membership, known as Direct Primary Care, involves paying a flat monthly fee for unlimited access to routine medical services. It eliminates insurance claims and offers personalized, longer visits, with costs ranging from $50 to $150 per month for adults. This model is best paired with a high-deductible health plan to cover hospitalizations and emergencies, providing affordable and accessible care.

A primary care membership is a healthcare arrangement where you pay a flat monthly fee directly to your primary care provider for unlimited access to routine medical services, bypassing insurance for everyday care. The industry term for this model is Direct Primary Care, or DPC. It gives you a real doctor who knows your name, answers your texts, and sees you the same day without a copay waiting on the other end. If you have ever felt rushed through a 15-minute appointment or avoided the doctor because of unpredictable costs, this model was built for you.

What is primary care membership and how does it work?

A primary care membership, formally called Direct Primary Care (DPC), is a flat monthly fee paid directly to your provider, typically ranging from $50–$150 for adults and $20–$49 for children. No insurance claims are filed for primary care services under this model. You pay your provider directly, and in return, you get access to a defined set of services without worrying about per-visit charges or deductibles.

The model removes the insurance company from the equation for routine care. That means your doctor spends time on you, not on paperwork. DPC practices maintain smaller patient panels of 400–800 patients, which is the structural reason you can actually get a same-day appointment. Traditional primary care practices often manage 2,000 or more patients per physician.

This is not a new concept, but it has grown significantly. The DPC model emerged as a direct response to the rushed, impersonal nature of fee-for-service medicine, where doctors are paid per visit and incentivized to see as many patients as possible. DPC flips that incentive entirely.

What services are typically included?

A standard primary care subscription service covers far more than most people expect. Here is what most memberships include:

- Unlimited in-person and virtual visits with no copay per visit

- Annual physicals and wellness exams included in the flat fee

- Chronic disease management for conditions like diabetes, hypertension, and asthma

- Telehealth and direct communication via text, phone, or video with your provider

- Minor in-office procedures such as sutures, skin biopsies, and wound care

- Discounted labs and medications negotiated directly by your provider

Typical DPC memberships include all of these services under one predictable monthly fee. That predictability is one of the most underrated primary care membership benefits. You know exactly what you are paying each month, and you know exactly what you get.

Pro Tip: Ask any prospective DPC provider for a full written list of included services before signing up. Some practices charge separately for procedures like biopsies or EKGs, so clarity upfront saves surprises later.

One often-overlooked advantage is the direct communication access. Average primary care visits in traditional US practices last about 18 minutes. DPC visits are longer and unhurried because your doctor is not racing to see the next patient in a packed waiting room. That extra time changes the quality of care you receive.

How does primary care membership pricing work?

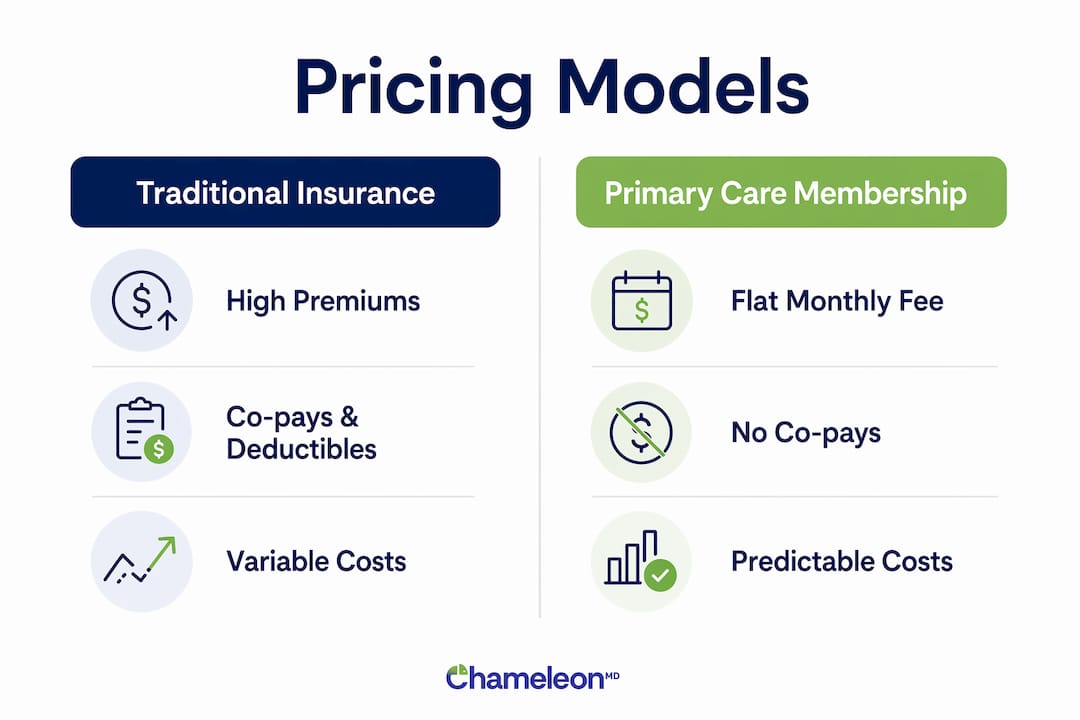

Pricing is one of the clearest advantages of this model. Monthly fees range from $50–$150 for adults, with family plans starting around $100 or more per month. Children’s fees are lower, typically $20–$49 per month. There are no deductibles, no copays, and no insurance claims filed for any primary care service.

Compare that to a traditional insurance plan, where a single specialist referral can trigger a $40–$60 copay, and a routine blood panel may cost $150 or more after your deductible. With a DPC membership, those labs are negotiated at wholesale prices and passed directly to you.

| Cost Factor | Traditional Insurance | Primary Care Membership |

|---|---|---|

| Monthly cost | $300–$600+ (premiums) | $50–$150 per adult |

| Per-visit copay | $20–$60 | $0 |

| Deductible | $1,000–$7,000+ | None for primary care |

| Lab work | Billed through insurance | Discounted wholesale rates |

| Billing complexity | High (claims, EOBs) | None |

One important nuance: DPC memberships are not insurance and do not qualify as ACA minimum essential coverage. Most people pair a DPC membership with a high-deductible health plan (HDHP) to cover hospitalizations, surgeries, and emergencies. If you have an HDHP, you can use Health Savings Account (HSA) funds to pay DPC fees, up to $150 per month for individuals or $300 per month for families.

Pro Tip: If your employer offers an HDHP with an HSA, ask HR whether your DPC membership fees qualify for HSA reimbursement. Many do, which effectively reduces your out-of-pocket cost further.

Employers are also catching on. Over 7,200 employers now offer DPC as an employee benefit, partially or fully subsidizing membership fees to reduce overall healthcare spending. That means your employer may already cover part of your membership cost.

Primary care membership vs. concierge medicine vs. traditional insurance

These three models are often confused, but they serve very different patients at very different price points.

Concierge medicine costs $1,500–$5,000 or more annually. It often still bills your insurance on top of the retainer fee and targets patients who want luxury services like 24/7 physician access, home visits, and specialist coordination. DPC costs $50–$150 per month and focuses on affordability and accessibility for everyday patients.

Traditional insurance is not a care model at all. It is a financial product. You pay premiums to an insurer, who then negotiates rates with providers and pays claims on your behalf. The result is administrative overhead, surprise bills, and a doctor who has 12 minutes to spend with you.

Here is how the three models compare on the factors that matter most to most patients:

| Factor | DPC Membership | Concierge Medicine | Traditional Insurance |

|---|---|---|---|

| Monthly cost | $50–$150 | $125–$417+ | $300–$600+ (premiums) |

| Insurance billing | No | Sometimes | Yes |

| Patient panel size | 400–800 | 300–600 | 1,500–2,500+ |

| Same-day access | Common | Common | Rare |

| Covers hospitalizations | No | No | Yes |

The key distinction for most consumers is this: DPC is the affordable primary care option that prioritizes access and transparency. Concierge medicine is DPC with a luxury price tag. Traditional insurance is a safety net for catastrophic events, not a primary care delivery model.

What to consider before choosing a primary care membership

A primary care membership is not the right fit for everyone, but it works exceptionally well for a specific type of patient. Before you sign up, work through these practical considerations:

- Confirm it is not your only coverage. A DPC membership does not cover hospitalizations, surgeries, or emergency care. You need separate major medical insurance for those events.

- Review the full service list. Not all DPC practices offer the same procedures. Some include mental health counseling; others do not. Ask specifically about chronic condition management if that applies to you.

- Check provider accessibility. The whole point of a membership is direct access. Ask how your provider handles after-hours questions and whether you can reach them by text or phone.

- Compare family plan pricing. If you have children, family plans starting around $100 per month can make DPC significantly more affordable than paying per-visit fees for each family member.

- Understand what is excluded. Specialist referrals, imaging, and hospitalizations are typically outside the membership scope. Know those boundaries before you commit.

Pro Tip: Search the DPC Frontier or AAFP’s DPC practice locator to find verified Direct Primary Care providers in your area. Not every practice that calls itself a “membership practice” follows the DPC model.

Personalized primary care solutions like DPC work best when you are moderately healthy, want a consistent relationship with one provider, and value predictable costs over comprehensive insurance coverage.

How do primary care memberships fit into the broader healthcare system?

The DPC model is not a fringe concept anymore. It has become a recognized part of how Americans access care, and its growth reflects real frustration with the traditional system.

| Trend | Data Point |

|---|---|

| DPC practices nationwide | Over 2,500 active practices |

| Employers offering DPC | 7,200+ as of 2026 |

| Typical patient panel size | 400–800 patients per physician |

| Average traditional visit length | ~18 minutes |

Physicians who adopt DPC report greater job satisfaction because they spend less time on insurance paperwork and more time on actual patient care. That satisfaction translates directly into better care quality for you. A doctor who is not burned out gives you a better appointment.

The most common pairing in 2026 is a DPC membership alongside a high-deductible health plan for catastrophic coverage. You handle routine care through your membership at a predictable monthly cost. The HDHP covers you if something serious happens. This combination gives you comprehensive coverage at a lower total cost than a traditional low-deductible plan in many cases.

Employers are adopting this pairing at scale. When a company offers DPC as a benefit, employees use primary care more consistently, catch problems earlier, and generate fewer expensive specialist and emergency room claims. That reduces costs for everyone.

Key takeaways

A primary care membership, formally called Direct Primary Care, is the most predictable and accessible way to manage routine healthcare costs without relying on traditional insurance billing.

| Point | Details |

|---|---|

| Flat monthly fee model | Adults pay $50–$150 per month with no copays or deductibles for primary care visits. |

| Services included | Unlimited visits, telehealth, annual physicals, chronic care, and discounted labs are standard. |

| Not a replacement for insurance | Pair your DPC membership with an HDHP to cover hospitalizations and emergencies. |

| Employer adoption is growing | Over 7,200 employers now offer DPC benefits, often subsidizing fees for employees. |

| DPC vs. concierge medicine | DPC is affordable and accessible; concierge medicine costs far more and often still bills insurance. |

Why i think DPC is the most underrated healthcare decision you can make

Most people I talk to assume that a primary care membership is either too good to be true or only for people without insurance. Both assumptions are wrong. The DPC model is not a workaround. It is a deliberate redesign of the doctor-patient relationship, and it works because it removes the one thing that makes primary care frustrating: the insurance company sitting between you and your doctor.

What surprises people most is the access. Texting your doctor directly and getting a response the same day sounds like a luxury. In a DPC practice, it is just how things work. That access changes your behavior as a patient. You ask questions earlier. You catch things before they become expensive problems.

The limitation people underestimate is the coverage gap. A DPC membership covers your everyday health needs exceptionally well. It does not cover the things that can financially ruin you, like a hospitalization or a surgery. If you sign up for DPC and cancel your major medical plan to save money, you are taking a real risk. The right move is to pair your membership with a lean HDHP and use your HSA to offset the membership cost.

The broader shift happening in US healthcare is real. More employers, more patients, and more physicians are choosing this model because it works better for everyone involved. If you have not looked into what a telehealth membership can actually include, you may be paying more than you need to for less access than you deserve.

— Vector

See how Chameleonhc makes primary care simple and affordable

Chameleonhc combines telehealth, urgent care, and primary care membership into one transparent model with no waiting rooms and no surprise bills. Whether you are managing a chronic condition like asthma or dealing with something that showed up today, Chameleonhc connects you with a licensed provider from your phone or computer, often the same day.

The pricing is clear, the access is real, and you do not need insurance to get started. If you are ready to see what a membership-based approach to primary care actually looks like, explore Chameleonhc’s plans and find the option that fits your life and your budget.

FAQ

What is a primary care membership in simple terms?

A primary care membership is a flat monthly fee paid directly to your doctor for unlimited access to routine care, with no copays or insurance billing for primary care services.

How does a primary care membership differ from health insurance?

A primary care membership covers routine and preventive care only. It is not insurance and does not cover hospitalizations, surgeries, or emergencies, so most members pair it with a separate major medical plan.

Is a primary care membership worth it for families?

Family plans typically start around $100 per month and include unlimited visits for covered members, making them a cost-effective option compared to paying per-visit fees for each family member under traditional insurance.

Can i use my HSA to pay for a primary care membership?

Yes. If you have a high-deductible health plan, you can use HSA funds to pay DPC membership fees, up to $150 per month for individuals or $300 per month for families.

What conditions does a primary care membership typically cover?

Most memberships cover chronic disease management, annual physicals, preventive care, minor procedures, and telehealth visits. Specialist referrals, imaging, and emergency care fall outside the standard membership scope.